As Climate Crisis returns to the new US administration agenda, negative emissions technologies (NETs) may find their implementation hindered by neoliberal financialization.

An earlier ACM story showed how Steve Keen’s critique of Nordhaus’s use of discounting climate change demonstrates that orthodox economics is incapable of accelerating innovation especially in the case of climate crisis. Cap and trade will not be even sufficient in the long-run.

Any one interested in the climate crisis MUST read this from @ProfSteveKeen Economic failures of the IPCC process | by Steve Keen | Jan, 2021 | Medium https://t.co/pMC27RZiTG— State of Flux (@stateoffluxHQ) January 12, 2021

But the main weaknesses with the IPCC’s methodology are firstly that, in economics, it exclusively selects Neoclassical economists, and secondly, because there is no built-in review of one discipline’s findings by another, the conclusions of these Neoclassical economists about the dangers of climate change are reviewed only by other Neoclassical economists. The economic sections of IPCC reports are therefore unchallenged by other disciplines who also contribute to the IPCC’s reports.

The Intergovernmental Panel on Climate Change (IPCC) is the premier international body collating the scientific assessment of climate change, and proposals for mitigation. A joint creation of the United Nations agencies the World Meteorological Organization (WMO) and the United Nations Environment Programme (UNEP), it brings together scientists from myriad disciplines to assess and summarize the current research on climate change, collating knowledge that is then used to inform governments and politicians. The scientists work on a volunteer basis.

Given the extent to which economists dominate the formation of most government policies in almost all fields, and not just strictly economic policy (Fourcade et al., 2015, Hirschman and Berman, 2014, Christensen, 2018, Lazear, 2000), the otherwise acceptable process by which the IPCC collates human knowledge on climate change has critically weakened, rather than strengthened, human society’s response to climate change. This is because, commencing with “Nobel Laureate” (Mirowski, 2020) William Nordhaus, the economists who specialise on climate change have falsely trivialized the dangers that climate change poses to human civilization.

[…]

In common with most of my peers in non-Neoclassical economics, I initially assumed that the answer was that he applied far too high a “discount rate” to future damages (Hickel, 2018). If you think that 99% of the economy would be destroyed in a century from now by the catastrophic effects of a 6°C increase in temperatures, but discount that back to today’s world at a rate of 7% p.a., you get the result that this collapse in future GDP is worth only 0.1% of today’s GDP — which is no big deal.

If this had been how Nordhaus had arrived at such low damage estimate, then the high discount rate could be challenged, but the rest of his analysis could potentially be sound. But our guess was wrong. Nordhaus explained why he used a high discount rate when he strongly criticised the lower discount rate used by theStern Review(Stern, 2007). It was not to reduce future catastrophic damages to trivial levels now, but because, if he used a low discount rate, then:

the relatively small damages in the next two centuriesget overwhelmed by the high damages over the centuries and millennia that follow 2200. (Nordhaus, 2007, p. 202. Emphasis added)

“Relatively small damages in the next two centuries”? How on Earth did he reach that conclusion? I found out,to my disgust, that he and his colleagues ignored or distorted the work of scientists, and instead made up their own trivial estimates of the economic damage from climate change. I have spent fifty years of my life being a critic of Neoclassical economics. Neoclassical work on climate change is by far the lowest grade work that I have read in that half-century.

[…]

As I detail inDebunking Economics(Keen, 2011), Neoclassical economics is riddled with false assumptions, because numerous theoretical and empirical requirements of the underlying theory have beenprovento be false. Rather than accepting that their initial beliefs were wrong, and then abandoning these beliefs to develop a richer, more complex theory, Neoclassical economists have clung to those beliefs by adding patently absurd assumptions to hide the contrary proofs.

[…]

Most politicians have studied some economics. Few have studied science, and they are therefore unable to read the science-based parts of the IPCC Reports. Most of their advisers — who actually read the reports for the politicians — are also trained in economics, rather than the sciences. Most political debate is about matters of economics, rather than science. The end result of all this is that, though scientists have led the study of climate change itself, economists have dominated public policy towards it. As Stephen De Canio put it in 2003:

it is undeniably the case that economic arguments, claims, and calculations have been the dominant influence on the public political debate on climate policy in the United States and around the world… It is an open question whether the economic arguments were the cause or only an ex-post justification of the decisions made … but there is no doubt that economists haveclaimedthat their calculations should dictate the proper course of action. (DeCanio, 2003, p. 4)

Because these economists, starting with William Nordhaus, trivialised the dangers of climate change, the policy response to climate change has also been trivial. Human civilisation may well not survive Neoclassical economics. It’s time it was eliminated, before it eliminates us.

I joined the very good folks who run this very good podcast to talk about job guarantee proposals, heterodox economics, climate change and lots of other things. Subscribe! https://t.co/lHcjyI3vfO

Deployment issues will become more complicated as policies get flummoxed by conflicts among national, regional, and state stakeholders among an ensemble of potential technologies with varying time, environmental impact, and cost constraints as identified by a new article on NETs.

Despite the ambitious long-term climate goals of theParis Agreement, there remains a distinctlack of successat ushering in immediate and sustained reductions in global CO2 emissions.

This cognitive dissonance has seen the topic of “negative emissions” – also known as “carbon dioxide removal” (CDR) – move into the limelight in climate science and policy discussions.

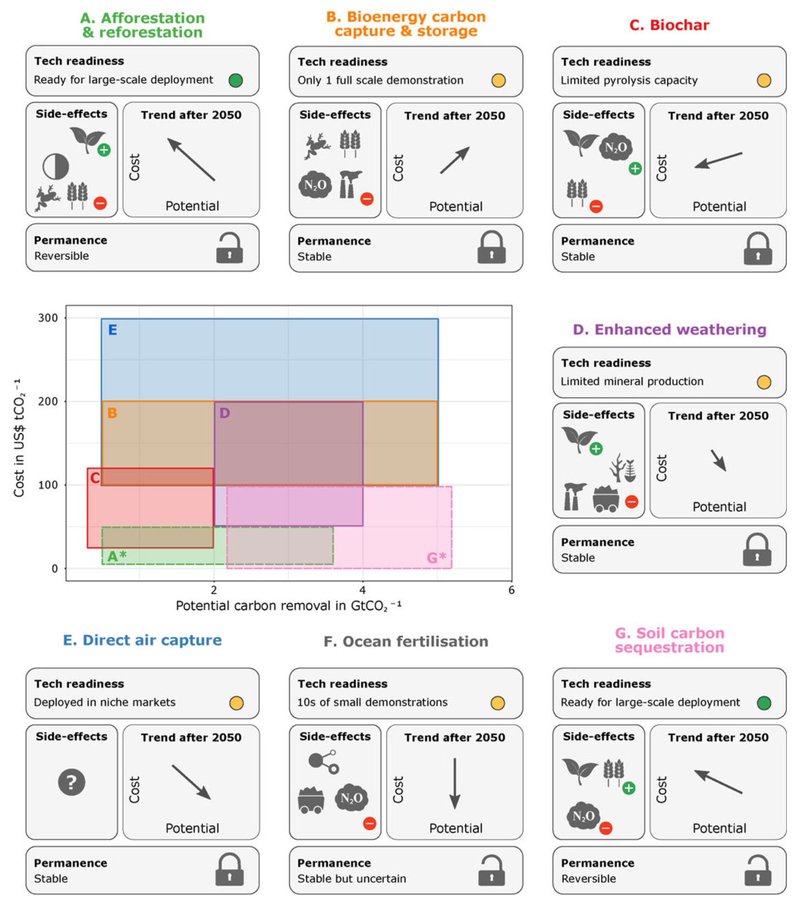

the maturity, potential, cost, side-effects and permanence of seven different NETs. The central panel shows how much CO2 each NET could potentially remove from the atmosphere (x axis) and at what cost (y axis). www.carbonbrief.org/…

In principle, negative emissions technologies NETs are feasible at a range of costs and with at least partially proven technology, but not at unlimited scale and not quickly. Many NETs also have high uncertainties regardingtheir wider impacts.

However, to ascertain the total potential of all NETs, it is not as simple as adding them together. Some NETs compete with one another – for land, water, bioenergy or safe geological storage, for example.

2. The literature on NETs is growing rapidly and diversifying

3. Modelling scenarios depend on negative emissions for 1.5C goal, but not for 2.0C

4. How society develops is crucial for the amount of NETs needed

5. Most NETs show potential for large-scale deployment, but all have limits

6. Adverse side effects of BECCS relate specifically to bioenergy

7. A big gap exists between R&D of NETs and actual deployment

In addition, realising the potential of each NET will require reliable institutions that incentivise good governance and practice across the globe.

This may constrain the ability to reach the higher end of deployment ranges – particularly for afforestation and soil carbon sequestration, where the cheapest options and largest potentials are often especially prominent in regions with weak institutions.

At the more expensive end, bioenergy with carbon capture and storage(BECCS) and direct air carbon capture and storage (DACCS) may have larger overall potentials and provide more reliable long-term storage, but show substantially higher costs and are currently in an earlier stage of the innovation process.

Our review also suggests that it would be difficult – and unwise – to try to meet the need to remove CO2 with one NET alone. It is, therefore, prudent to think about a NETs “portfolio”, with each deployed at more modest scales and, consequently, with more manageable risks.

In fact, there may be a “natural order“ of NETs deployment that arises from considerations of costs, potentials, effectiveness, availability as well as safe and permanent storage.

For example, an initial phase-in could use some of the land-based options, such as afforestation or soil carbon sequestration, which are readily available, comparatively cheap, and more easily reversible, but suffer from saturation in the long-run and are harder to manage on a large scale. Technological options, such as BECCS and DACCS, could be phased in later and provide the required additional potentials once they are ready.

Moral suasion is not enough as the long term trend towards greater financialization may defeat all attempts at climate change beyond NETs. There could be speculative innovation bubbles under such financialization, especially with an oncoming post-pandemic recession.

In the American experience, increased financialization occurred concomitant with the rise ofneoliberalismand the free-market doctrines ofMilton Friedmanand theChicago School of Economicsin the late twentieth century. Various academic economists of that period worked out ideological and theoretical rationalizations and analytical approaches to facilitate the increasedderegulationof financial systems and banking.

Financialization may be defined as “the increasing dominance of the finance industry in the sum total of economic activity, of financial controllers in the management of corporations, of financial assets among total assets, of marketized securities and particularly equities among financial assets, of the stock market as a market for corporate control in determining corporate strategies, and of fluctuations in the stock market as a determinant of business cycles” (Dore 2002).

Neoliberalism’s proclivities for concentration and profit while projecting deregulation will become greater as NETs present expanded market opportunities even in portfolios of varied technologies and production schedules.

Ineconomics,economic rentis any payment to an owner orfactor of productionin excess of the costs needed to bring that factor into production. In classical economics, economic rent is any payment made (including imputed value) or benefit received for non-produced inputs such as location (land) and for assets formed by creating officialprivilegeover natural opportunities (e.g.,patents). In themoral economyofneoclassical economics, economic rent includes income gained by labor or state beneficiaries of other “contrived” (assuming the market is natural, and does not come about by state and social contrivance) exclusivity, such as labor guilds and unofficial corruption.

In the moral economy of the economics tradition broadly, economic rent is opposed toproducer surplus, ornormal profit, both of which are theorized to involve productive human action. Economic rent is also independent ofopportunity cost, unlikeeconomic profit, where opportunity cost is an essential component. Economic rent is viewed as unearned revenue[1]while economic profit is a narrower term describing surplus income earned by choosing between risk-adjusted alternatives. Unlike economic profit, economic rent cannot be theoretically eliminated by competition because any actions the recipient of the income may take such as improving the object to be rented will then change the total income tocontract rent. Still, the total income is made up ofeconomic profit(earned) plus economic rent (unearned).

Rents also represent transaction costs that will hinder NETs, especially in environmental commodities with multiple markets requiring regulation and coordination. Activism might have diminishing effects and frustrating delays in terms of mobilizing state and corporate action.

Commodity trading firms occupy a central position in global supply chains and their activities have been associated with financial instability, social upheaval and manifold forms of ecological devastation. This paper examines these companies in the context of debates regarding corporate financialization. We find that since the 2003-2011 commodity boom, trading firms have become less financialized in terms of the source of their profits as they have shifted away from financial activities. However, they have become more financialized in terms of the destination of profits, with dividend and share repurchase commitments reaching new heights after 2015. In view of this finding, we inquire into whether trading firms’ growing commitment to shareholder payouts will encourage them to continue to prioritize short-term returns, or whether instead these

firms’ linkages to financial markets will lend clout to financial activists concerned by the long-term environmental and social consequences of their operations. Ultimately, we find several sources of commodity trader resilience which insulate them from shareholder resolutions and divestment campaigns aimed at curbing ecological destruction and human rights abuses in their supply chains. We accordingly suggest that pressures from activist investors must be complemented with more wide-ranging efforts to defend living systems across the planet.

x

In our latest for @RIPEJournal Joseph Baines and I examine some of the most important but under-researched corporations in the world today: the commodity trading firms. How do we make sense of these firms and their role in ecological devastation? [1/8] https://t.co/VYyOX7bpGe

Some claim that financialization has encouraged a short-term outlook in the sector, with dire social and ecological consequences. But evidence for these claims is patchy, so part of our research involved mapping financialization metrics for the top commodity trading firms [2/8]

The evidence is mixed. For example, we find that commodity traders have become less financialized in the source of profits (financial income), but more financialized in the destination of profits (shareholder payouts) [3/8]

Does the trading firms’ growing commitment to shareholder payouts encourage them to prioritize short-term returns? Or do their linkages to financial markets lend clout to financial activists concerned by the environmental and social consequences of their operations? [4/8]

We argue that these firms are shielded from financial activist pressures due to the predominance of private ownership structures, the dispersion of holdings in the their bonds as well as company deleveraging and shadow banking activities [5/8]

Also, voting data for the 'big three' asset managers in the commodity sector show that they almost always vote in favour of management resolutions for dividends and buybacks, and they almost always vote against resolutions aimed at environmental and social governance [6/8]

Our conclusion: we need much more than divestment campaigns and shareholder resolutions to push these firms onto a more sustainable pathway [7/8]

A climate scientist spent years trying to get people to pay attention to the disaster ahead. His wife is exhausted. His older son thinks there’s no future. And nobody but him will use the outdoor toilet he built to shrink his carbon footprint. https://t.co/M0NYtVHV8J— ProPublica (@propublica) January 31, 2021

The second point to stress is more directly related to the movement for the climate and the environment (the red-green universe) as it exists in the West. In recent years there has been a rapprochement in Europe and in the United States between the political imaginary of the traditional social-issues left, heir to the workers’ movement, and that of political ecology. Admittedly, the compromise between these two worlds remains quite fragile, to the extent that the alignment between the exploitation of humans and of nature is debatable. But a strategic pact is nonetheless taking shape around reactivating economic interventionism, in a play on references to the postwar period. The Green New Deal, in its significantly varied American and European versions, does not yet structure investment plans that are both capable of meeting the challenge and truly rooted in social justice objectives, but it has imposed itself as the common ground of the Western left.

[…]

The ecology movement should therefore agree to talk about strategy, conflict, and security; it should present itself as a dynamics of building a political form that assumes the idea of power without scaling back on social and democratic demands. In fact, these demands can only be achieved if they are invested into specifically political reflections and practices. But for this to be possible, we have to leave behind our tendency toward moral depoliticization, because we no longer have a monopoly on the critique of the fossil development paradigm. A new arena is emerging, and we have no choice but to launch ourselves into it.